An SME can have its accounts up to date and still not know where it is making money.

It may file its taxes correctly, prepare its annual accounts, monitor bank movements and invoices, and still be unable to answer one important question with confidence: Which part of the business is generating margin, and which part is simply consuming resources?

That is where cost accounting comes in.

Not as another accounting exercise. As a management tool.

Because a business needs to know how much it has spent. But it also needs to understand what caused that cost, which activity absorbed it, which client required it, and what real margin remains afterwards.

In this article, we explain how to implement a cost accounting system in an SME in Spain from a practical, finance-led perspective. We focus on the decisions a finance team or management team needs to make: what to measure, how to allocate costs, which mistakes to avoid, and how to turn analysis into pricing, efficiency and profitability decisions.

The difference lies in how the information is used. An accounting figure records what happened. A good cost accounting system helps explain why it happened, how it affected margin and what management can do to correct it.

That is why cost accounting should be integrated into a broader model of financial control for companies in Spain, where costs, margins, budgeting and reporting work under the same logic.

Cost accounting is not financial accounting with more detail

Financial accounting follows a legal, accounting and tax logic. It records transactions, supports the preparation of annual accounts and ensures compliance with the applicable accounting framework.

In Spain, companies must keep their accounts in accordance with the Spanish General Accounting Plan. However, certain companies may apply the General Accounting Plan for SMEs, a simplified version of the same accounting framework.

This option is available to companies that meet specific thresholds for total assets, turnover and average number of employees over two consecutive financial years.

Cost accounting serves a different purpose.

It answers management questions such as:

- What margin does each client leave after internal hours have been absorbed?

- Which product appears profitable when only direct cost is considered, but becomes less attractive once indirect costs are included?

- Which business line is subsidising another?

- What is the minimum price required to avoid destroying margin?

- Which part of the structure is underused?

- Is the variance driven by volume, price, productivity or sales mix?

The difference is clear:

Financial accounting shows the result.

Cost accounting explains how that result was formed.

The common mistake: confusing the tool with the cost model

Many SMEs already have enough tools: accounting software, ERP systems, shared spreadsheets, BI dashboards or monthly reports.

But a tool does not create a cost accounting system by itself.

A company may have cost centres, analytical tags and visual dashboards, and still not know whether the margin by client, product or project is reliable. The problem appears when the rules are not defined before measurement begins.

Each department then interprets the data in its own way. Indirect costs are allocated based on turnover because it is the easiest option. Exceptional expenses get mixed into operating margin. Internal hours are not allocated correctly. Labour cost is calculated without including the full employer cost. And, in the end, the analytical model does not reconcile with the income statement.

When that happens, management stops trusting the data.

That is why a cost accounting model should not start with the tool. It should start with the architecture: what you want to measure, which costs will be allocated, which criteria will be applied, which information will be excluded, who validates the data and how it connects with financial reporting.

Step 1: define the cost object before calculating anything

The first mistake is to ask: “What costs do we have?”

The right question is different: What do we want to measure profitability against?

That defines the cost object.

A cost object may be:

- A product.

- A product family.

- A service.

- A project.

- A client.

- A branch.

- A store.

- A sales channel.

- A business line.

- A production unit.

- A subsidiary or group company.

Choosing the wrong cost object distorts the whole system.

A professional services firm does not need the same model as a manufacturing company. An SME working on a project basis needs to measure hours, time allocation, variances and scope. A business with inventory needs to control purchase cost, transformation cost, storage, turnover and obsolescence. An e-commerce business needs to look at product, logistics, returns, discounts, payment gateways and marketing by channel.

This is not just a technical decision. It is a strategic one.

Step 2: separate traceable, allocable and non-assignable costs

The traditional split between direct and indirect costs is often too limited for SMEs with a certain level of complexity.

It is more useful to work with three levels.

Traceable costs

These are costs that can be clearly linked to a cost object.

Examples:

- Raw materials for a product.

- Merchandise sold.

- Hours allocated to a project.

- Specific transport for an order.

- Commissions on a specific sale.

- Licences used by a particular team.

These costs should be assigned directly, without allocation.

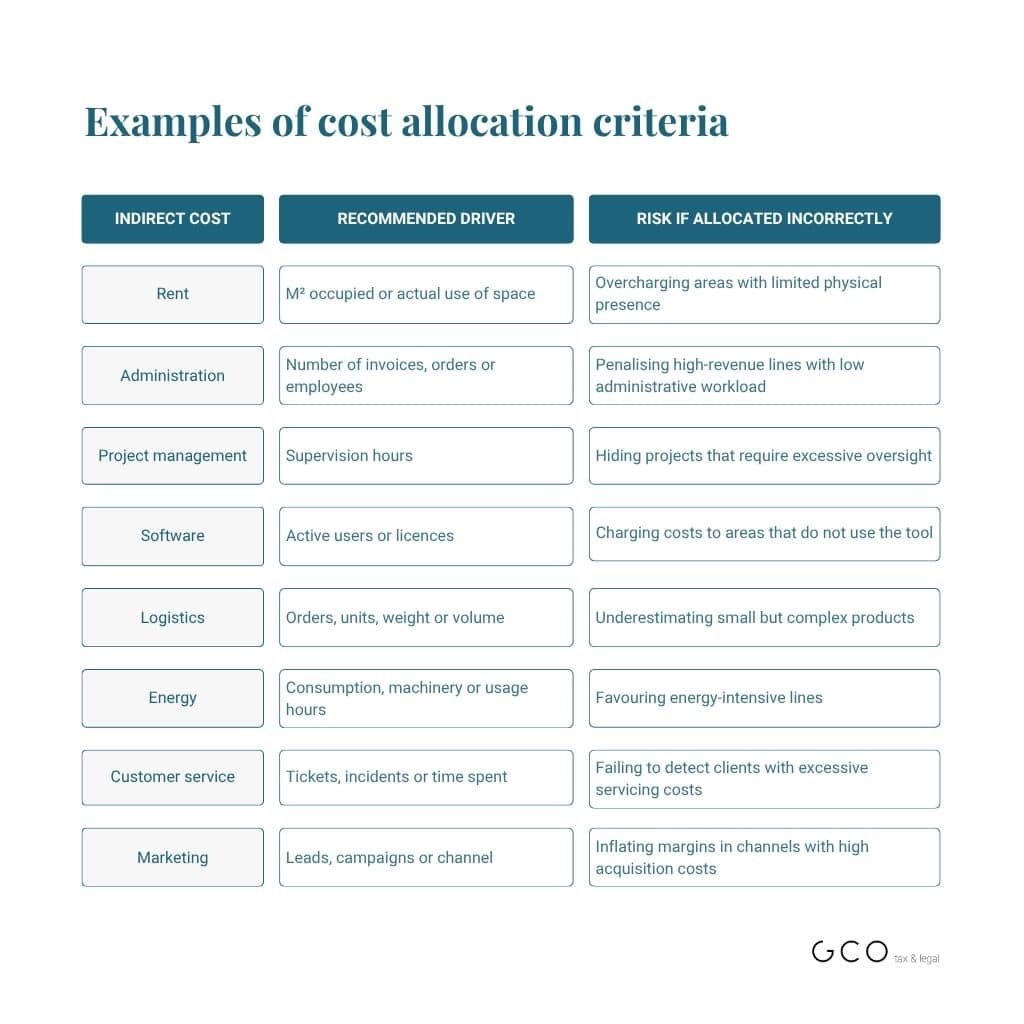

Allocable costs

These cannot be linked directly, but they can be allocated using a reasonable criterion.

Examples:

- Rent based on square metres.

- Administration based on the number of invoices.

- Software based on users.

- Technical management based on estimated hours.

- Energy based on consumption or machinery usage.

- Logistics based on the number of orders or units moved.

This is where cost allocation methods come in.

Costs that should not be assigned for decision-making purposes

Some costs exist, but it may not make sense to allocate them to a product, client or project if they do not add clarity.

Examples:

- Exceptional expenses.

- Penalties.

- Non-recurring costs.

- Restructuring costs.

- Certain corporate expenses.

- Internal projects not linked to current sales.

Allocating everything may look rigorous.

But sometimes it makes the analysis less useful.

A good model does not allocate every cost by default. It allocates the costs that help management make better decisions.

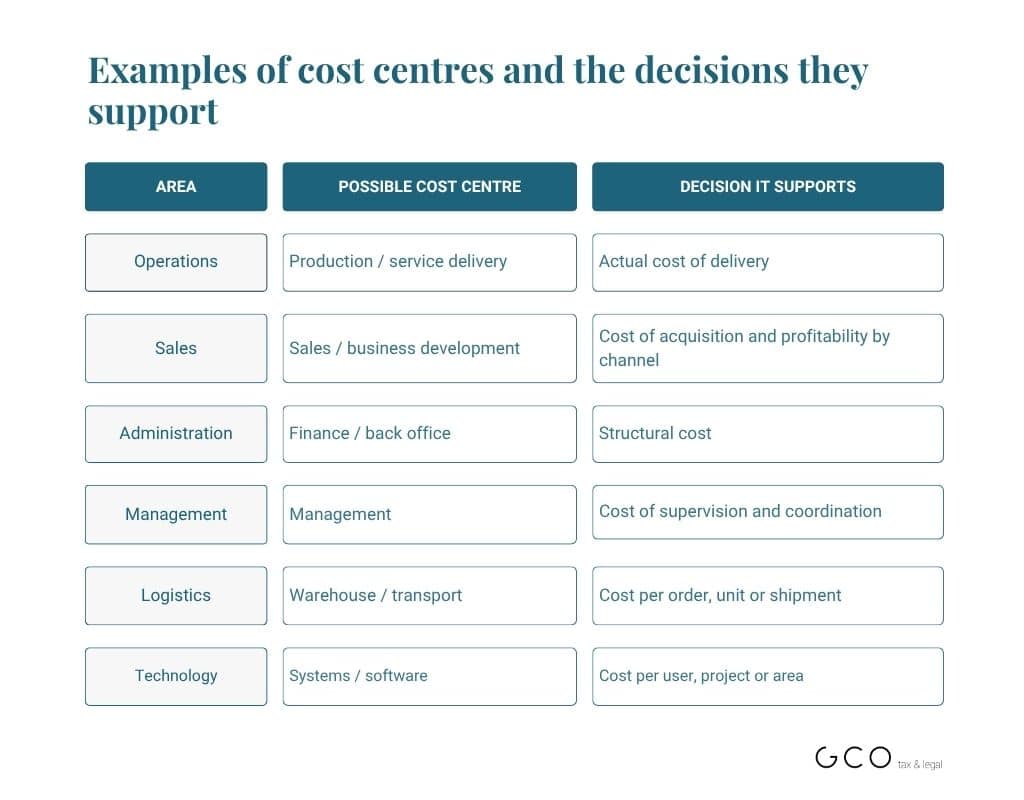

Step 3: design cost centres without creating unnecessary bureaucracy

Cost centres help organise the business.

But too many cost centres can slow it down.

An SME can start with a simple structure.

The rule is straightforward:

Create a cost centre only if someone will use that information to make a decision.

If it does not change any decision, it probably does not need to be measured separately.

Step 4: choose cost allocation methods that reflect real resource consumption

Cost allocation methods are the criteria used to allocate indirect costs.

This is one of the areas where SMEs most often get it wrong.

The easiest criterion is usually turnover. But it is not always the fairest.

One client may generate high revenue and consume few resources. Another may generate less revenue but require more meetings, more deliverables, more changes, more issues and more support.

If both absorb costs based on turnover, the analysis will be misleading.

The question is not:

Which driver is easiest?

The question is:

Which variable best explains the consumption of that resource?

Step 5: decide whether you need direct costing, full costing, ABC or standard costing

Not all cost models serve the same purpose.

An SME with a certain level of complexity should understand at least four approaches.

Direct costing

Direct costing only considers direct and variable costs to calculate contribution margin.

It is useful for short-term decisions:

- Accepting or rejecting orders.

- Assessing promotions.

- Prioritising products.

- Analysing break-even point.

- Deciding whether a sale helps cover fixed structure.

It is useful, but incomplete if used in isolation.

Full costing

Full costing includes direct costs and a reasonable share of indirect costs.

It is used to assess full profitability by product, client or business line.

It is more demanding because it requires clear allocation criteria. If those criteria are weak, the full margin will also be weak.

Activity-Based Costing, or ABC

Activity-Based Costing allocates costs based on activities: orders processed, changes requested, issues resolved, support hours, machine set-ups, shipments or returns.

It is particularly useful when products, clients or services consume resources very differently.

It is not always necessary to implement a full ABC model. Many SMEs can apply selective ABC to the processes that distort margin the most: logistics, support, commercial administration or project management.

Standard costing

Standard costing defines an expected cost per unit, hour, product or process. The actual cost is then compared against that standard.

It is useful for controlling variances in:

- Purchase price.

- Material consumption.

- Productivity.

- Labour efficiency.

- Capacity usage.

- Wastage.

- Non-productive time.

Standard costing does not replace actual cost.

It provides a reference point for detecting variances.

Step 6: do not confuse accounting margin with decision-making margin

This point often separates a basic analysis from a truly useful one.

Not all costs are relevant for all decisions.

To decide whether to increase prices, you need full cost and commercial elasticity.

To decide whether to accept a one-off order, contribution margin may be enough if there is spare capacity.

To decide whether to close a business line, you need to know which costs would truly disappear and which would remain in the structure.

To decide whether to outsource, you need to compare the real internal cost with the external cost, but also assess operational risk, quality, dependency and management capacity.

The same cost figure may be useful for one decision and irrelevant for another.

That is why it is important to distinguish between:

- Accounting cost: The cost recorded in the financial accounts.

- Operating cost: The cost linked to the actual running of the business. It helps explain how much it costs to produce, sell, deliver a service or keep an activity running.

- Incremental cost: The additional cost the company would incur if it made a specific decision. For example, accepting an additional order, opening a new channel or producing more units.

- Avoidable cost: The cost that would disappear if an activity, product, client or business line were removed.

- Sunk cost: A cost that has already been incurred and cannot be recovered, even if the company changes course. It should not drive future decisions, although it often does.

- Opportunity cost: The value of the alternative the company gives up when it chooses one option over another.

- Cost of unused capacity: The cost of resources the company has available but is not using, such as idle machinery, underused staff, unused space or structure prepared for a higher level of activity.

An SME does not need to turn this into an academic exercise.

But it does need to avoid expensive decisions based on misread margins.

Step 7: include normal capacity and under-activity

When a company manufactures, delivers services or develops projects, it does not always use its full capacity.

It may have idle machinery, underused staff, non-billable hours, oversized warehouses or teams prepared for a volume that has not yet arrived.

If all that idle capacity is allocated to active products or projects, unit cost rises artificially.

And that can lead to the wrong conclusion.

The ICAC Resolution on production cost sets out criteria for determining production cost and states that the allocation of indirect production costs should be based on the level of use of normal capacity, excluding inactivity or under-activity costs from production cost.

Translated into management terms:

you should not load a profitable product with the cost of an underused structure if that underuse is a capacity or volume issue.

That is why these concepts should be separated in management reporting:

- Product margin: Shows whether the product is profitable based on its revenue and the costs that genuinely relate to it.

- Absorbed structural cost: Reflects the reasonable share of fixed costs the product should bear based on the company’s normal capacity.

- Cost of under-activity: Shows the cost of unused capacity, such as idle machinery, underused staff, oversized facilities or resources prepared for a volume that has not yet materialised.

- Operating result: Brings together product margin, absorbed structure and the impact of under-activity to show the real operating performance of the business.

This separation helps management understand where the problem lies.

The product may have margin, but the company may lack volume. The price may be right, but the structure may be oversized. Or unit cost may be increasing because the company is not using its capacity sufficiently.

Without this reading, the company may blame the product when the real issue is structure or level of activity.

Step 8: build a bridge between financial accounting and the cost model

A cost accounting model should reconcile with the accounts.

Not line by line, necessarily, but at a logical level.

If the income statement shows €500,000 in personnel expenses, the internal model cannot work with €430,000 without explaining the difference.

There needs to be a bridge between both worlds.

On one side, financial accounting shows the result recorded by the company. On the other, the cost model reorganises that information to explain how profitability is generated by product, client, project, cost centre or business line.

That bridge should make it clear which part of the accounting result has been included in the cost analysis, which adjustments have been made and which amounts have been separated because they do not help measure operating profitability.

For example, an exceptional expense may not be allocated to a business line so it does not distort its margin. Or part of the structure may be separated as under-activity cost because it relates to unused capacity. Or certain accruals may be adjusted to make monthly comparisons more consistent.

This reconciliation builds trust.

Without it, the cost model becomes a parallel system that is hard to defend. And when management does not understand where the figure comes from, it stops using it.

Step 9: turn the model into monthly reporting

Cost accounting should not sit in a file that is reviewed once a year.

It should feed into monthly management reporting.

A useful report should include:

- Margin by product, client, project or business line.

- Variance against budget.

- Variance against standard cost.

- Non-recurring costs.

- Capacity used.

- Under-activity.

- Profitability by channel.

- Clients with excessive servicing cost.

- Evolution of fixed costs.

- Margin alerts.

- Recommended actions.

But the aim is not to add more indicators to the management report.

The aim is for every data point to answer a specific question: where margin is being made, where it is being lost, which cost has deviated and what decision should be taken before the next close.

That is why cost accounting should be integrated into the company’s financial control model in Spain.

If costs, budgets, margins and reporting work separately, management receives disconnected pieces of information.

If they work under the same logic, management gets a complete view of the business.

Cost KPIs: measure only what helps decision-making

An SME does not need 30 cost indicators.

It needs a small number of well-defined KPIs, reviewed with discipline.

In a cost accounting model, KPIs should help answer specific questions:

- Is product margin decreasing?

- Are some clients consuming more resources than they pay for?

- Does the cost per productive hour support the current fee structure?

- Is the variance against standard cost driven by purchasing, productivity or capacity usage?

- Is under-activity distorting unit cost?

The key is not to create a more complete dashboard.

It is to choose indicators that connect costs, margins and decisions.

That is why it is useful to separate the two levels. Cost accounting should define the operational KPIs that explain margin. Financial reporting should then integrate them with other indicators such as gross margin, net margin, EBITDA, liquidity, ROI, ROA or inventory turnover.

To go deeper into this second layer, you can read GCO’s guide on financial KPIs for accounting control.

The value of a KPI is not in the measurement itself.

It lies in how well it informs the next business decision.

Seven mistakes that distort profitability

Allocating all indirect costs based on sales.

It is convenient. But it can penalise the lines that generate the most revenue and protect the ones that consume the most resources.

Failing to separate recurring and non-recurring costs

A one-off expense can artificially depress monthly margin. If it is not separated, structural decisions may be made based on temporary noise.

Treating all clients as if they required the same effort

Two clients with the same revenue can have very different margins if one requires more meetings, urgent requests, changes, special deliveries or support.

Miscalculating labour cost

Gross salary is not the real cost.

Employer cost, social security, benefits, tools, training, absenteeism, holidays, supervision and non-productive hours must also be considered.

Not measuring idle capacity

If under-activity is not separated, the company may think the product is expensive when the real issue is that the structure was sized for higher volume.

Not documenting the rules

Without written rules, every monthly close reopens the same debate.

A good model should include a short manual covering:

- Cost object.

- Cost centres.

- Allocation criteria.

- Responsibilities.

- Update frequency.

- Exclusions.

- Treatment of exceptional items.

- Reconciliation with accounting.

Creating a model that is too complex

Too much detail can kill the system.

If updating the model takes too long, the team will stop doing it. It is better to start with an 80/20 model that management actually uses every month.

How to implement cost accounting in 90 days

Days 1–30: diagnosis and design

Objective: understand how margin is generated.

Tasks:

- Review the income statement.

- Identify relevant business lines, products, projects or clients.

- Analyse direct and indirect costs.

- Detect parallel control systems.

- Review how prices are calculated.

- Define cost objects.

- Design cost centres.

- Decide which costs will be allocated and which will be excluded.

Result: cost and profitability map.

Days 31–60: allocation rules and first model

Objective: build an operating model.

Tasks:

- Define cost drivers.

- Document cost allocation methods.

- Calculate real labour cost.

- Create the cost centre structure.

- Load historical data.

- Build the first analytical income statement.

- Reconcile with financial accounting.

- Validate results with management.

Result: first margin model by cost object.

Days 61–90: reporting, review and decisions

Objective: turn the model into a management tool.

Tasks:

- Create a monthly report.

- Set a management accounting close calendar.

- Review variances.

- Identify low-margin lines.

- Separate under-activity costs.

- Propose price, process or structure adjustments.

- Define responsibility for updates.

Result: cost accounting system integrated into monthly financial control.

FAQ about cost accounting in Spain

Is cost accounting only useful for manufacturing companies?

No. It is often associated with factories, production or inventory, but it can also add significant value in service businesses, consulting firms, professional practices, agencies, e-commerce companies, multi-site businesses and companies working on a project basis.

The key question is not whether the company manufactures.

The key question is whether it needs to know which client, service, product, channel or business line generates real margin.

If we already have an ERP or accounting software, do we still need a cost accounting model?

Probably, yes.

An ERP can record data, but it does not always answer the management questions that directors need. To be useful, it must be properly configured: cost centres, cost objects, allocation criteria, responsibilities, reporting frequency and reconciliation with financial accounting.

The tool helps.

But the company defines the model.

How do I know whether my margin by client or product is reliable?

A margin is reliable when you can explain where it comes from.

That means knowing which costs have been assigned directly, which indirect costs have been allocated, which cost allocation methods were used and which expenses were excluded to avoid distorting the analysis.

If the margin depends on undocumented criteria, poorly reviewed automatic allocations or data that does not reconcile with the income statement, it should be reviewed before decisions are made.

Does cost accounting help with pricing?

Yes, but it should not be the only factor.

A good cost model helps calculate the minimum price, understand the real margin and detect products or services that are being sold below full cost. But pricing should also consider the market, competition, perceived value, commercial elasticity and positioning strategy.

Cost sets the floor.

It does not necessarily set the final price.

How often should the cost model be reviewed?

At a minimum, it should be reviewed monthly if it is used for management purposes.

A monthly review makes it possible to detect variances, margin changes, non-recurring costs, under-activity or allocation issues before they affect the accumulated result for the year.

The allocation criteria should also be reviewed whenever the business structure changes: new lines, new channels, more staff, supplier changes, openings, closures or significant investments.

Who should be responsible for the cost accounting model?

Finance should lead it, but finance cannot build it alone.

Operations, sales, management, logistics, HR or project managers should be involved whenever their data affects margin. Otherwise, the model may be technically correct but operationally unrealistic.

Cost accounting works best when finance validates the logic and the business areas provide operational context.

What are the warning signs that the cost model is not working?

There are several clear warning signs: management does not trust the data, each department calculates margins differently, indirect costs are always allocated based on turnover, the model does not reconcile with financial accounting or reports arrive too late to support decisions.

There is also a less obvious sign: the model produces data, but it does not change any business conversation.

Turn your costs into decisions

If your company has data but cannot turn it into clear decisions on margin, pricing and profitability, the problem may not be accounting alone.

It may be the control model.

At GCO, we help companies in Spain organise their financial information, improve accounting processes, implement cost accounting models and build management reporting that is useful for decision-making through our financial advisory services in Barcelona.

The first step is not to add more complexity.

It is to review what information you need in order to make better decisions.